What Employee Health Benefits Are Actually Tax-Deductible for My Business and How Much Can I Save?

Quick Answer:

Many employee health benefits are tax-deductible for a business, including employer-paid health insurance premiums, dental and vision premiums, certain health reimbursement arrangements, employer HSA contributions, and some wellness or employee assistance programs when they are set up correctly. In most cases, these costs are treated as ordinary business expenses or employee benefit expenses.

But here is the part owners need to hear clearly: tax-deductible does not mean free.

A deduction lowers your taxable business income. It does not give you back the full amount you spent. If your business spends $20,000 on deductible employee health benefits and your effective tax rate is 25%, the rough tax savings may be about $5,000. The business still spent $20,000. It just reduced the after-tax cost.

Some very small employers may also qualify for the Small Business Health Care Tax Credit, which can be more powerful than a deduction. But the credit has strict rules, usually involving employer size, average wages, SHOP coverage, and the percentage of employee premiums the business pays.

The Simple Version: The IRS Rewards Structure, Not Guesswork

Health benefits can be one of the better tax-advantaged ways to compensate employees.

That does not mean the IRS lets owners make it up as they go.

A properly structured group health plan can give the business a deduction while giving employees a valuable benefit that is often excluded from their taxable income. That is why health benefits are such a big deal in compensation planning. The employer may get a business deduction. The employee may receive coverage without treating the full value as taxable wages.

That is the clean version.

The messy version is when a business starts reimbursing random medical bills, paying personal premiums informally, giving cash “for health insurance,” or treating owners exactly like rank-and-file employees without checking entity rules.

That is where the headaches start.

The tax code is usually friendlier when the benefit is formal, documented, and run through the right plan structure.

It gets much less friendly when the owner says, “Just bring me the receipt and I’ll pay you back.”

The Big Rule: Deductible Does Not Mean Free

Let’s get the math out of the way first.

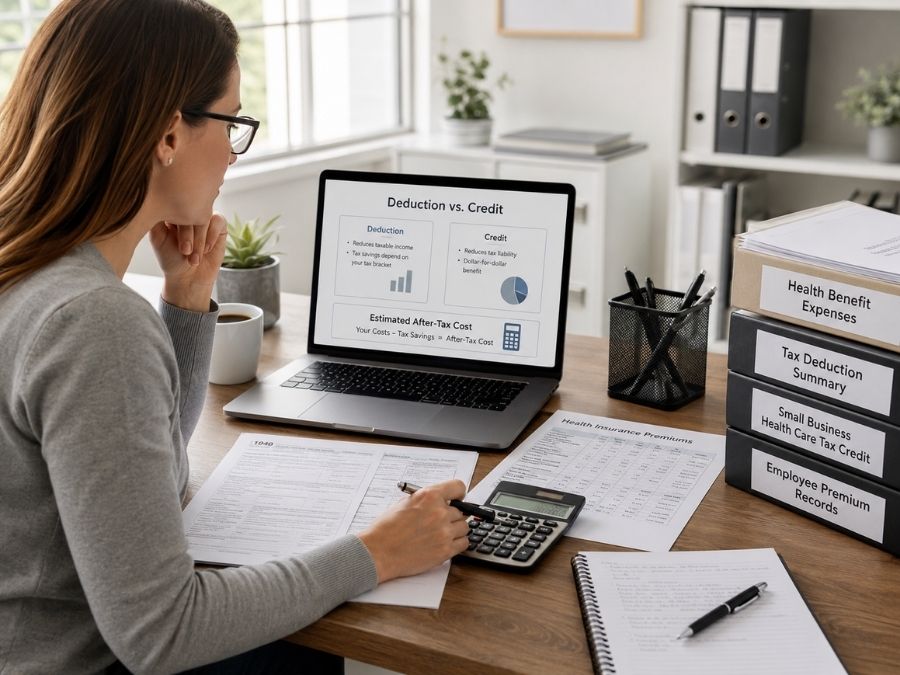

A tax deduction reduces taxable income. A tax credit reduces tax owed. Those are not the same thing.

If your business spends $10,000 on deductible health benefits and your effective tax rate is 21%, your rough tax savings may be $2,100.

You did not save $10,000.

You spent $10,000 and reduced your tax bill by about $2,100.

That means your after-tax cost is roughly $7,900.

That is still real money. It is just less painful than spending the same amount on something that is not deductible.

Deduction vs. Credit: The Difference Owners Actually Need

| Tax Benefit | What It Does | Simple Example |

|---|---|---|

| Deduction | Reduces taxable business income. | A $10,000 deduction at a 25% effective tax rate may save about $2,500 in taxes. |

| Credit | Reduces the tax bill directly. | A $5,000 tax credit may reduce taxes owed by $5,000. |

| Tax-Free Employee Benefit | Lets the employee receive value without ordinary taxable wages in many cases. | Employer-paid group health coverage is often more valuable than the same dollars paid as taxable cash. |

This is where owners get tripped up.

A deduction is useful.

A credit is usually stronger.

A tax-free employee benefit can be stronger still, because the employee may receive more value than they would from the same amount paid through payroll.

What Employee Health Benefits Are Usually Tax-Deductible?

Most standard employee health benefit costs are generally deductible when they are ordinary, necessary, properly documented, and tied to employees rather than personal owner spending.

Common deductible health-related benefits may include:

- Employer-paid group health insurance premiums

- Employer-paid dental insurance premiums

- Employer-paid vision insurance premiums

- Employer contributions to Health Savings Accounts

- Employer-funded Health Reimbursement Arrangements

- Qualified Small Employer Health Reimbursement Arrangements

- Employee Assistance Programs

- Certain wellness program costs

- Administrative fees for group health plans

- COBRA administration costs

- Telehealth or virtual care programs, if structured as part of the benefit plan

- Certain disability insurance premiums, depending on structure and tax treatment

That list looks generous.

But the words “depending on structure” matter.

Health benefits are not just about whether the expense sounds medical. They are about how the plan is set up, who receives the benefit, whether the benefit is discriminatory, whether the cost is properly documented, and how the business is taxed.

The same $300 can be clean, taxable, nondeductible, or a compliance problem depending on how it is paid.

That is why structure matters more than good intentions.

The Most Common Deductible Health Benefit: Group Health Insurance

For most small businesses, group health insurance is the main deductible health benefit.

The employer pays part or all of the employee’s premium. That employer-paid portion is generally treated as a business expense. Employees often pay their share through payroll, sometimes on a pre-tax basis if the company has a properly structured Section 125 cafeteria plan.

This is the classic setup.

The business gets a deduction for the employer contribution. The employee gets access to coverage. The benefit may help recruiting and retention. Everyone understands what the plan is.

The cleaner the setup, the better.

The plan documents, payroll deductions, employee handbook, carrier invoices, and accounting records should all match. If the owner pays premiums from one account, reimburses some employees informally, and lets managers explain eligibility from memory, the tax savings may not be the only issue anymore.

That is an audit trail problem.

And nobody enjoys rebuilding an audit trail after the fact.

Dental and Vision Premiums

Dental and vision premiums are often deductible too when offered as employee benefits through a proper plan.

These benefits usually cost less than major medical coverage, which makes them attractive to small businesses trying to build a benefits package in stages. Employees also understand them quickly. Nobody needs a long seminar to understand why dental and vision coverage can be useful.

The tax treatment is usually straightforward when the employer pays the premium as part of a group benefit arrangement.

The trouble starts when the employer is not consistent.

If one employee gets reimbursed for personal dental coverage because the owner likes them, while another employee in the same role gets nothing, that is not a benefits strategy. That is a side deal.

Side deals are where tax and HR problems tend to meet.

HSA Contributions

Health Savings Accounts can be powerful, but they come with rules.

An employer can contribute to an eligible employee’s HSA if the employee is covered by a qualifying high-deductible health plan and meets the other HSA eligibility requirements. For the business, employer HSA contributions are generally deductible as employee benefit costs or compensation-related expenses, depending on the setup.

For employees, the value can be excellent because HSA money may go in tax-free, grow tax-free, and come out tax-free when used for qualified medical expenses.

That is the good news.

The caution is that HSA contributions are not unlimited. Annual limits apply. Eligibility rules matter. Employees who are not HSA-eligible should not receive HSA contributions. And owners should not assume that every health plan with a high deductible automatically qualifies.

Ask before contributing.

Do not guess.

HRAs and QSEHRAs

Health Reimbursement Arrangements, or HRAs, allow employers to reimburse employees for certain medical expenses under a formal arrangement. A QSEHRA, or Qualified Small Employer Health Reimbursement Arrangement, is designed for eligible small employers that do not offer a traditional group health plan.

That can be useful for smaller employers that want to help employees with health costs without sponsoring a full group health plan.

But again, this is not “hand me your receipt and I’ll Venmo you.”

A compliant HRA or QSEHRA needs plan documents, employee notices, reimbursement procedures, and limits. The arrangement has to follow the rules. Done correctly, reimbursements may be deductible for the employer and tax-advantaged for the employee.

Done casually, it can become taxable income or a compliance problem.

Generosity does not fix bad structure.

Wellness Programs and Employee Assistance Programs

Wellness programs and Employee Assistance Programs can also be deductible business expenses when they are properly connected to employee benefits, workplace health, or employee support.

This might include mental health support, counseling access, stress management resources, smoking cessation programs, health screenings, fitness-related programs, or other wellness initiatives.

But this category gets fuzzy.

A formal EAP through a provider is different from randomly paying for one employee’s gym membership. A structured wellness program is different from buying a massage chair and calling it healthcare. Some wellness benefits may be taxable to employees depending on what is provided and how.

The cleaner approach is to ask three questions:

Is this a real employee benefit?

Is it offered under a clear policy?

Is the tax treatment documented correctly?

If the answer is no, slow down.

Disability Insurance Premiums

Disability insurance deserves special attention because the tax result depends heavily on who pays and how the premiums are treated.

If the employer pays disability insurance premiums and deducts them, the benefit payments may be taxable to the employee if the employee later becomes disabled and receives benefits. If employees pay premiums with after-tax dollars, disability benefits may be tax-free to the employee.

That is the tradeoff.

This does not mean one structure is always better. It means the business should explain the tax consequences clearly and set up payroll correctly.

Disability coverage can be a strong employee benefit.

Just do not let someone sell it as “tax-free” without explaining which side of the transaction they mean.

Tax Treatment Snapshot

| Benefit Type | Usually Deductible for Employer? | Usually Tax-Free to Employee? | Watch For |

|---|---|---|---|

| Group health insurance premiums | Yes, when properly structured | Often yes | Eligibility rules, plan documents, payroll setup |

| Dental and vision premiums | Often yes | Often yes | Consistent eligibility and plan documentation |

| Employer HSA contributions | Generally yes | Generally yes, within limits | HSA eligibility and annual contribution limits |

| HRA or QSEHRA reimbursements | Generally yes | Often yes if compliant | Formal plan documents and reimbursement rules |

| EAP benefits | Often yes | Often yes, depending on structure | Scope of benefits and taxability |

| Wellness programs | Often yes | Depends on benefit type | Cash rewards, gym reimbursements, and discrimination rules |

| Disability premiums | Often yes | Depends on who pays and tax treatment | Taxation of future disability benefits |

| Cash health stipends | Usually deductible as wages | Usually taxable wages | Payroll taxes, ACA, ERISA, and plan compliance |

This table is the practical version.

The deduction is only one part of the story.

The real question is whether the benefit is deductible, tax-free to the employee, compliant, and worth the administrative work.

The Cash Stipend Trap

This is where a lot of small businesses get sloppy.

An owner does not want to set up group health insurance yet. So they tell employees, “We’ll give you $300 a month for health insurance.”

That sounds generous.

But if it is just paid as cash, it is usually taxable wages. The employee owes taxes. The employer owes payroll taxes. And depending on how it is described or administered, the arrangement may create health plan compliance problems.

A taxable stipend may still be allowed in some cases.

But do not confuse it with a tax-free health benefit.

Those are different things.

If the business wants to reimburse individual health premiums or medical expenses in a tax-advantaged way, it should look at formal arrangements like QSEHRAs or other compliant reimbursement models with a benefits advisor or tax professional.

Do not freelance this one.

The IRS has seen every version of “we thought it was just a stipend.”

How Much Can a Business Actually Save?

The savings depend on the business tax rate, entity type, payroll tax treatment, whether the benefit is tax-free to employees, and whether the company qualifies for any credits.

But the basic deduction math is simple:

Deductible benefit cost × effective tax rate = estimated tax savings.

Here is a rough example.

If a business spends $36,000 per year on deductible employee health benefits and has a 25% effective tax rate, the estimated tax savings may be about $9,000.

That means the after-tax cost is roughly $27,000.

The business did not avoid the cost.

It reduced the net cost.

That is still valuable.

But it is not a rebate.

Estimated Tax Savings Examples

| Annual Deductible Health Benefit Cost | Effective Tax Rate | Rough Tax Savings | Estimated After-Tax Cost |

|---|---|---|---|

| $10,000 | 21% | $2,100 | $7,900 |

| $25,000 | 25% | $6,250 | $18,750 |

| $50,000 | 25% | $12,500 | $37,500 |

| $100,000 | 30% | $30,000 | $70,000 |

These are simplified examples.

They do not replace tax planning.

They do show the basic idea: a deductible benefit reduces the pain, not the purchase price.

The Small Business Health Care Tax Credit

Some small businesses may qualify for the Small Business Health Care Tax Credit.

This matters because a credit can be more valuable than a deduction.

Eligible small employers may qualify for the credit if they cover at least 50% of full-time employee premium costs and have fewer than 25 full-time equivalent employees. The credit may be worth up to 50% of premium costs paid by qualifying small employers, or up to 35% for qualifying nonprofit employers.

That sounds excellent.

But the credit is not available to every small business with health insurance. Eligibility depends on factors such as employee count, average wages, employer premium contribution, and often coverage through the SHOP Marketplace. The credit also phases down as the employer gets larger or average wages rise.

In other words, it can be powerful.

But it is narrow.

Worth checking.

Not worth assuming.

Deduction vs. Small Business Health Care Tax Credit

| Scenario | Deduction | Credit |

|---|---|---|

| How it works | Reduces taxable income | Reduces tax owed directly |

| Who may use it | Many businesses with deductible health benefit costs | Only eligible small employers that meet specific rules |

| Value | Depends on tax rate | Potentially up to 50% of eligible premiums for qualifying small businesses |

| Complexity | Usually simpler | More rules, calculations, and eligibility limits |

| Planning note | Common baseline tax benefit | Worth checking if employer is small enough and pays enough of premiums |

If you qualify for the credit, talk to your tax professional.

If you do not qualify, the deduction may still help.

Just do not mix up the two.

They are different tools.

Entity Type Matters More Than Owners Think

This is where a lot of small business owners get surprised.

Employee health benefits for rank-and-file employees are often straightforward. Owner benefits can be different.

A C corporation owner-employee may be treated differently from an S corporation shareholder. Partners in a partnership have different rules. Sole proprietors have their own self-employed health insurance deduction rules. More-than-2% S corporation shareholders often need special payroll handling for health insurance premiums.

This is not the place to copy what another business owner does.

Two companies can spend the same amount on health coverage and get different tax results because they are taxed differently.

Before assuming the owner’s health premiums are deductible the same way as employee premiums, check the entity rules.

That one detail can change the entire tax treatment.

Special Owner Tax Issues to Flag

| Business Type | Watch For |

|---|---|

| Sole proprietor | May use self-employed health insurance deduction if eligible, subject to rules. |

| Partnership | Partner health coverage is often handled differently from common-law employee coverage. |

| S corporation | More-than-2% shareholder health insurance usually requires special W-2 treatment. |

| C corporation | Owner-employees may have more straightforward employer plan treatment, but compensation reasonableness still matters. |

| LLC | Tax treatment depends on whether the LLC is taxed as sole proprietorship, partnership, S corp, or C corp. |

The business structure matters.

The payroll setup matters.

The plan documents matter.

That is why this article can explain the map, but your CPA needs to drive the final route.

Comprehensive Record-Keeping Checklist

If you want the deduction, keep the evidence.

That sounds obvious.

It is not always how small businesses operate.

Keep these records organized throughout the year:

- Primary insurance carrier invoices and premium settlement records

- Signed health plan documents and defined employee eligibility classifications

- Trailing payroll deduction records and automated accounting logs

- Formally executed Section 125 cafeteria plan contracts, if applicable

- Internal HSA contribution logs and detailed HRA/QSEHRA reimbursement folders

- Written employee open-enrollment notices and formal board approvals

- Proof of premium payments

- Employee notices and benefit election records

- Accounting entries showing how benefits were classified

- Documentation for any wellness, EAP, disability, or stipend-related benefit

Do not wait until tax season to reconstruct this.

Benefits records should be clean all year.

If your bookkeeper, payroll provider, broker, and CPA all have different numbers, the problem is not tax law.

The problem is your process.

Common Tax Mistakes With Employee Health Benefits

Most tax mistakes in this area come from informality.

The owner is trying to help.

The office manager is trying to move fast.

The payroll provider is only processing what they were told.

Then the tax professional sees the mess six months later.

Watch for these common mistakes:

- Treating taxable cash stipends as tax-free health benefits.

- Reimbursing individual health premiums without a compliant plan.

- Forgetting payroll tax treatment on cash health payments.

- Offering benefits only to favored employees or owners.

- Ignoring special rules for S corporation shareholders, partners, or sole proprietors.

- Failing to keep plan documents.

- Deducting expenses without clean proof of payment.

- Assuming the business qualifies for the Small Business Health Care Tax Credit without checking the rules.

- Using one employee’s medical needs to decide benefit eligibility.

- Mixing personal owner medical costs with employee benefit expenses.

That last one is a big one.

Personal medical costs do not become business expenses just because the owner runs them through the company account.

That is not tax planning.

That is bad bookkeeping with confidence.

The Strategic Tax Savings Checklist

Work through these ten diagnostic checkpoints in chronological order before finalizing your deduction strategy:

- Identify the core benefit type.

Clarify whether the cost is group insurance, dental, vision, HSA funding, HRA/QSEHRA reimbursement, disability coverage, wellness support, EAP access, or cash wage additions. - Confirm your structural framework.

Ensure the benefit is bound by a legal policy, plan document, reimbursement arrangement, or carrier contract. - Isolate employees from owners.

Check whether corporate entity status requires special W-2 shareholder adjustments, partner treatment, or self-employed health insurance handling. - Determine the employee tax consequence.

Map out whether the value counts as tax-free employee benefit value or standard taxable wages. - Verify the employer business deduction.

Ensure the expense matches the ordinary and necessary threshold and is tied to legitimate employee benefit costs. - Calculate payroll tax liabilities.

Assess whether your payment setup triggers additional FICA, unemployment, withholding, or payroll reporting costs. - Evaluate tax credit eligibility.

Review whether your headcount, average wages, premium contribution, and coverage arrangement let you claim the Small Business Health Care Tax Credit. - Project your accurate after-tax costs.

Run the formula: Deductible Cost × Effective Tax Rate = True Savings. - Secure your permanent evidence trail.

Catalog invoices, carrier records, payroll deductions, reimbursement approvals, notices, and accounting entries. - Schedule an annual professional audit.

Sync with your CPA to adjust for changing headcounts, ownership structure, tax rules, benefit design, and employee eligibility.

This is not busywork.

This is how you avoid turning a good benefit into a tax-season cleanup project.

The Bottom Line: Health Benefits Can Save Taxes, But They Still Need Structure

Employee health benefits can absolutely create tax savings for a business.

Employer-paid health insurance, dental, vision, HSA contributions, HRAs, QSEHRAs, EAPs, and some wellness programs may be deductible when properly structured. Employees may also receive major value when benefits are excluded from taxable wages.

But the savings are not automatic.

The business needs the right plan structure, clean payroll treatment, consistent eligibility rules, and documentation. Owner benefits need extra care. Cash stipends need caution. Tax credits need qualification, not wishful thinking.

The best way to think about it is simple.

Health benefits can reduce the after-tax cost of taking care of employees.

They do not erase the cost.

And they do not forgive sloppy setup.

Next Step for Owners

Pull your last 12 months of health benefit spending and separate it into categories: premiums, dental, vision, HSA contributions, reimbursements, stipends, wellness costs, disability premiums, and administrative fees.

Then ask your CPA or tax advisor three questions:

- Which of these costs are deductible?

- Which payments are taxable to employees?

- Do we qualify for the Small Business Health Care Tax Credit?

If you cannot answer those three questions clearly, your tax savings may be smaller than you think, or your compliance risk may be bigger than it looks.

Frequently Asked Questions About Tax Deductions for Employee Health Benefits

Is employer-paid health insurance tax deductible for a small business?

Generally yes. When a business pays part or all of employee health insurance premiums through a properly structured group health plan, that cost is typically treated as a deductible business expense. The deduction reduces taxable business income, which lowers the tax bill. But the deduction does not give the money back. If the business spends $30,000 on deductible health premiums and has a 25% effective tax rate, the rough tax savings may be about $7,500. The business still spent $30,000. It just made the after-tax cost closer to $22,500. The deduction is real and useful. It is not a reimbursement.

How much can a small business actually deduct for employee health benefits?

There is no fixed dollar cap on the employer deduction for employee health insurance premiums the way there is for some other benefit types. The business can generally deduct what it actually spends on qualifying employee health benefits, as long as the costs are ordinary, necessary, properly documented, and tied to employees rather than personal owner expenses. What limits the deduction is not a ceiling but a set of rules about who qualifies, how the plan is structured, whether the costs are documented, and whether owner benefits are handled correctly for the entity type. A sole proprietor, S corporation shareholder, and C corporation owner-employee can all spend the same amount and end up with different deduction results because the rules apply differently.

What is the Small Business Health Care Tax Credit and does my business qualify?

The Small Business Health Care Tax Credit is a federal tax credit that can reduce a qualifying small employer’s tax bill directly, which makes it potentially more valuable than a deduction. Eligible employers may receive a credit worth up to 50% of premiums paid, or up to 35% for qualifying nonprofit employers. But the eligibility rules are strict. The business generally needs to have fewer than 25 full-time equivalent employees, pay average wages below a certain threshold, cover at least 50% of full-time employee premium costs, and obtain coverage through the SHOP Marketplace, which is the Small Business Health Options Program. The credit is also only available for two consecutive taxable years, which is a limitation many owners miss when they first hear about it. Worth checking with a tax professional, but do not assume qualification without reviewing the rules carefully.

Can I give employees cash instead of health insurance and still deduct it?

Yes, but the tax treatment is probably not what the owner is hoping for. Cash paid to employees in place of health benefits is generally taxable wages. That means the employee owes income taxes on it, the employer owes payroll taxes on it, and it does not carry the same tax-free value that properly structured health coverage can provide. A deductible cash payment is not the same as a tax-free health benefit. If the goal is to help employees with health costs in a tax-advantaged way, formal arrangements like a QSEHRA or other compliant reimbursement model may be worth exploring with a benefits advisor. Paying cash informally and calling it a health benefit is one of the most common small business compliance mistakes in this area.

Are HSA contributions tax deductible for the business?

Yes, employer contributions to eligible employees’ Health Savings Accounts are generally deductible as a business expense. For the employee, the value can be significant because HSA funds may go in tax-free, grow tax-free, and come out tax-free when used for qualified medical expenses. When HSA contributions are made through a Section 125 cafeteria plan, there may also be FICA tax savings for both the employer and employee, which adds to the overall tax efficiency. But eligibility rules apply. The employee must be covered by a qualifying high-deductible health plan and meet other HSA requirements. Annual contribution limits also apply. Do not contribute to an employee’s HSA without confirming eligibility first.

Does my business entity type affect how health insurance deductions work?

Yes, and this is where a lot of owners get surprised. Rank-and-file employee health benefits are often handled similarly across entity types. Owner benefits are where the rules diverge. A sole proprietor may use the self-employed health insurance deduction under a different set of rules. A more-than-2% S corporation shareholder typically needs health insurance premiums run through W-2 wages with special payroll treatment. Partners in a partnership have their own rules. A C corporation owner-employee may have more straightforward group plan treatment. Two business owners can spend the same amount on health coverage and get different tax results because they are taxed differently. The entity type is not a detail. It is part of the calculation.

What records does a business need to keep to deduct employee health benefits?

The business needs records that connect the expense to a legitimate employee benefit and show the cost was actually paid. That usually means carrier invoices and premium payment records, plan documents and employee eligibility records, payroll deduction records showing how employee contributions were handled, Section 125 cafeteria plan documents if applicable, HSA contribution logs or HRA reimbursement records if relevant, employee notices and benefit election records, and accounting entries showing how the expense was classified. Benefits records should be organized throughout the year, not reconstructed at tax time. If the bookkeeper, payroll provider, broker, and CPA all have different numbers, the problem is not tax law. The problem is the process.

What are the most common tax mistakes businesses make with employee health benefits?

The most common mistakes come from informality and assumptions. Paying taxable cash stipends and treating them as tax-free health benefits. Reimbursing individual health premiums without a compliant plan structure. Forgetting payroll tax treatment on cash health payments. Applying benefits inconsistently or only to favored employees. Ignoring special rules for S corporation shareholders, partners, or sole proprietors. Failing to maintain plan documents. Mixing personal owner medical costs with employee benefit expenses. Assuming the business qualifies for the Small Business Health Care Tax Credit without checking the eligibility rules. The pattern is usually the same. The owner or manager is trying to be helpful, the process is informal, and the tax professional sees the problem months later when it is harder to fix. Good intentions do not create compliant benefits. Structure does.